Packaging: an opportunity not to be wasted

How Circular Design, Strategic Partnerships, and Digital Transformation can turn trash into treasure

Welcome to Climate Drift - the place where we dive into climate solutions and help you find your role in the race to net zero.

If you haven’t subscribed, join here:

Hey there! 👋

Skander here.

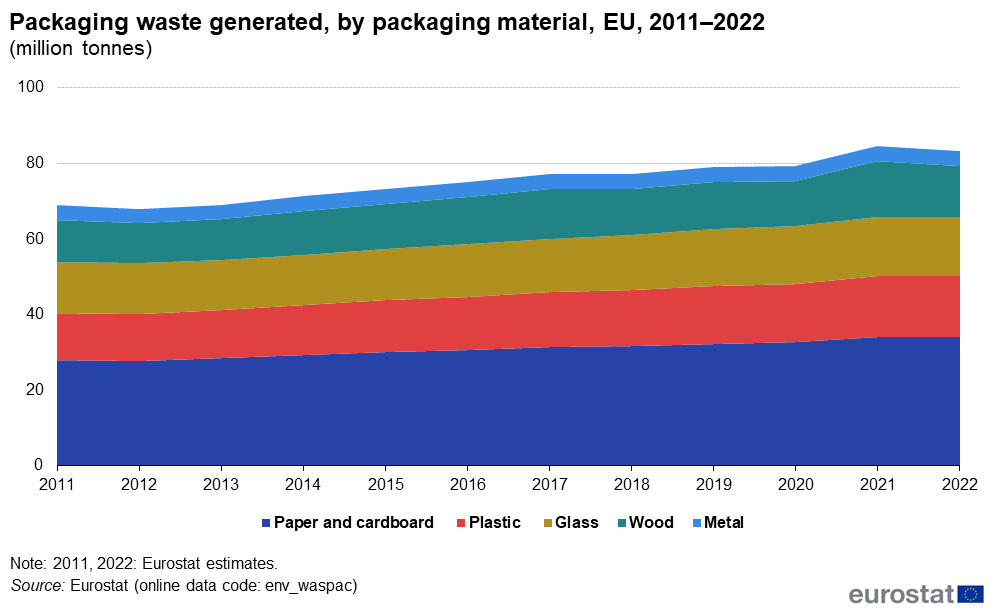

Today, we’re diving into a topic that’s hiding in plain sight but has massive implications for both businesses and the environment: packaging waste. Every day, the European Union generates 228,000 tonnes of packaging waste, about the weight of 23 Eiffel Towers. And while recycling exists, a huge amount of packaging material still gets burned, buried, or lost in the environment.

But here’s the thing: this isn’t just a sustainability problem; it’s a business opportunity. Companies that figure out how to close the loop, designing for recyclability, securing secondary materials, and leveraging partnerships, will have a real competitive advantage.

To unpack this issue (pun intended) driftie Laura presents a new framework to rethink the packaging value chain, covering design, waste collection, and recycling, while breaking down the critical capabilities companies need to build to unlock value. Whether you’re a brand looking to manage Extended Producer Responsibility (EPR) costs, a climate investor seeking opportunities, or a recycling company navigating a shifting landscape, this one’s for you.

🌊 Let’s dive in

🚀 Want to make an impact?

The 4th cohort of our accelerator launches in March, and applications are still open (but spots are limited). If you’re ready to fight climate change, don’t wait:

But first, who is Laura?

Laura Miller is a strategy and operations leader with 10 years of experience (Shopify and PwC Consulting), partnering with senior management and cross-functional teams to transform operations & go-to-market strategies into a key driver of revenue growth, cost reduction, and organizational alignment. She has an MBA from INSEAD, and she strongly believes in the opportunity to improve the sustainability of legacy sectors through digital transformation.

She currently leads the Business Planning & GTM Strategy function for Shopify EMEA, after having first developed and scaled Shopify EMEA’s commercial processes and cross-functional operating model. As a Manager at PwC Consulting, she advised multi-billion dollar businesses in the Retail & Consumer and Transportation & Logistics sectors on digital supply chain transformation.

Packaging: an opportunity not to be wasted

The European Union generates 228K tonnes of packaging waste every day - the equivalent weight of 23 Eiffel Towers! The virgin material demand for packaging is significant: the EU packaging sector (annual turnover of €370B) currently consumes 40% of plastics and 50% of paper produced in the EU).

However, the majority of value from packaging is lost when the waste is burned, sent to landfill, downcycled into other materials, or ends up in the environment.

This article will present a new framework to understand the packaging value chain; its current constraints; new capabilities required to drive value; and real life examples of partnerships between legacy players and climate tech companies to improve value capture.

Companies who establish a circular model for their materials can gain a competitive advantage as they can secure their material supply, customize recycled materials to their needs, and drive customer engagement.

The packaging value chain can unlock significant value if new capabilities are established to address constraints at three main stages of the value chain: packaging design; packaging waste collection & sortation; and recycling & material resale.

Building and scaling these capabilities will require close collaboration (and funding) among players across the value chain, and in this spirit, this article will provide insights to multiple stakeholder groups.

Brands: understand the root cause of recycling challenges and opportunities to decrease their Extended Producer Responsibility (EPR) costs and secure material supply for their future packaging

Climate investors: discover ideas about how to help their portfolio companies grow by driving partnerships and data exchange across the value chain

Waste management and recycling companies: a framework to identify opportunities to grow revenue and decrease operational costs through these new capabilities

Climate tech companies: a holistic view of the packaging value chain to identify opportunities for partnerships and ideas about how to quantify the financial benefits of their solutions to customers

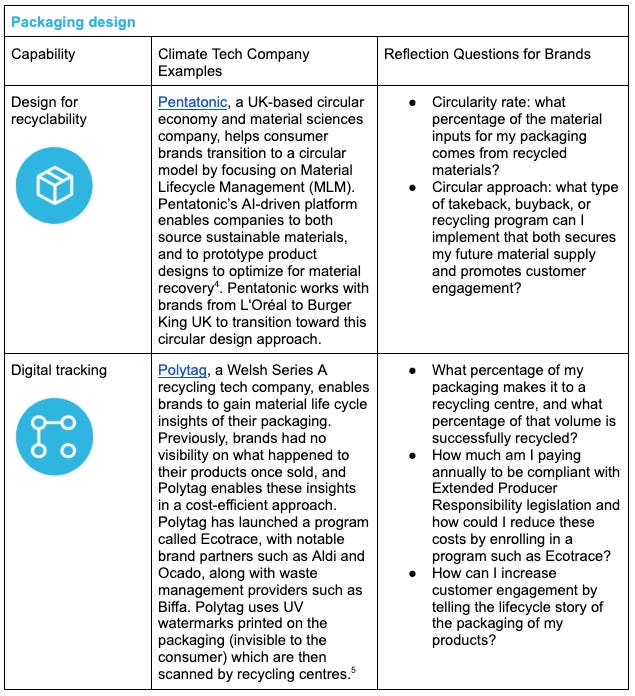

Packaging Design

About 80% of packaging's environmental impact is determined during design, creating both an opportunity and challenge for brands. While companies can significantly reduce their environmental footprint through design choices, there is a ‘Catch 22’: recycled materials remain costly until supply increases, and supply won't grow until more companies design recyclable packaging. Designers can address this by prioritizing recyclability, material longevity, and resale value alongside traditional metrics like cost and durability, while also reducing material usage.

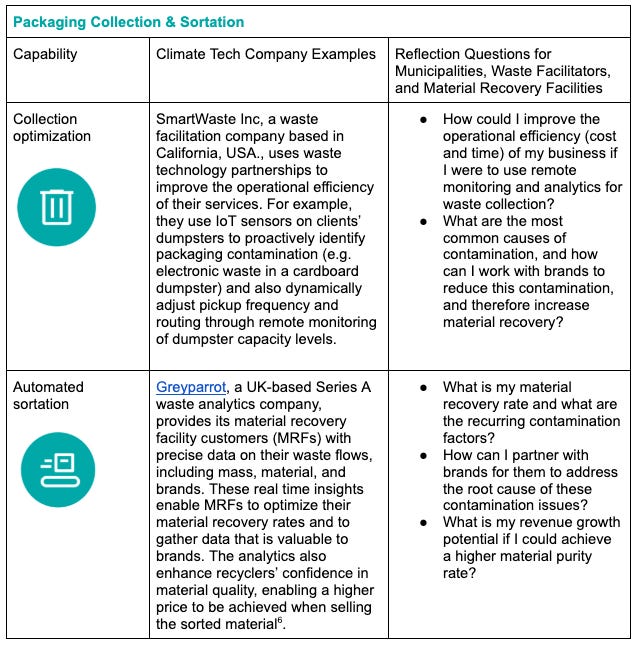

Stage 2: Packaging Collection & Sortation

Waste collectors, waste facilitators, and Material Recovery Facilities (MRFs) play a crucial role in collecting packaging waste and sorting the packaging material into specific waste streams (e.g. PET, HDPE, Paper, Aluminum), which can then be sold to recycling facilities. Increasing the volume of packaging waste that is both collected and sorted is instrumental to increasing the volume of recycled materials available for packaging.

Packaging waste collection varies by jurisdiction, and is typically divided into single or dual stream collection. The challenge of single stream collection is that all packaging is placed in the same bin, increasing the chances of material contamination, as well as the work (and cost) required to identify and sort the materials accurately.

The impact of the first stage (packaging design) has a direct impact on the quality of outputs and recovery rates based on: a) materials used; b) ease of being able to separate different materials used in a piece of packaging. For plastics, PET (polyethylene terephthalate) and HDPE (high-density polyethylene), #1 and #2 within the chasing arrows symbol, are most widely recycled.

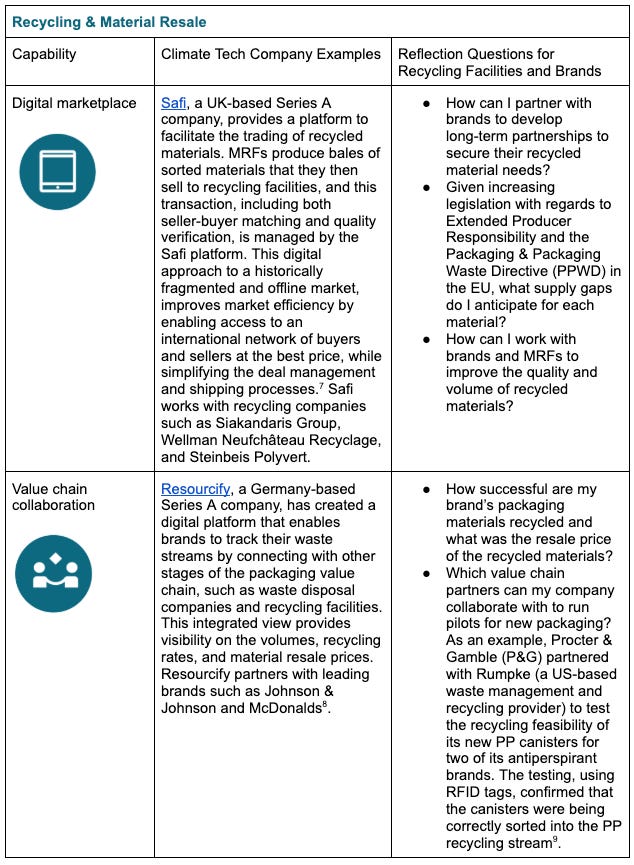

Stage 3: Recycling & Material Resale

As noted earlier, packaging designers should seek to use packaging materials that are commercially attractive to recycle. Similar to other markets in the economy, there needs to be customer demand before MRFs and recyclers will invest in producing different recycled materials. Historically, the sales process between MRFs and recycling companies has happened ‘offline’, presenting an opportunity to digitize the space and drive partnerships between MRFs, recycling facilities, and brands on an international scale.

As evidenced above, there is an incredible opportunity ahead to transform the packaging value chain through partnerships among brands, legacy players in the recycling and waste management industry, climate tech companies with the pioneering technologies to support new capabilities, and funding from investors to enable these companies to scale.

Brands who prioritize increasing the circularity rate of materials in their packaging value chain will benefit financially in the long term and will establish a strategic advantage as their material supply will be secured. The environment will benefit too as fewer virgin materials will be used to create new packaging materials.

Interested in learning more or chatting about opportunities in the packaging value chain & circular economy? Connect with Laura!

| A guest post by

|

Great primer on this problem. Love the granularity and simple explanations to help understand all the players and moving parts. Also appreciate hearing about climate tech companies building solutions.